Taking Money from your Limited Company

New HMRC Consultation puts the Director's Loan Account into Focus

A proposal to introduce a legal requirement on businesses to report transactions between close companies and their participators to HM Revenue and Customs has just been announced.

Close companies are those controlled by five or fewer participators, or by any number of participators who are directors and a participator is a person with a share or interest in the capital or income of a company; usually they are the shareholders.

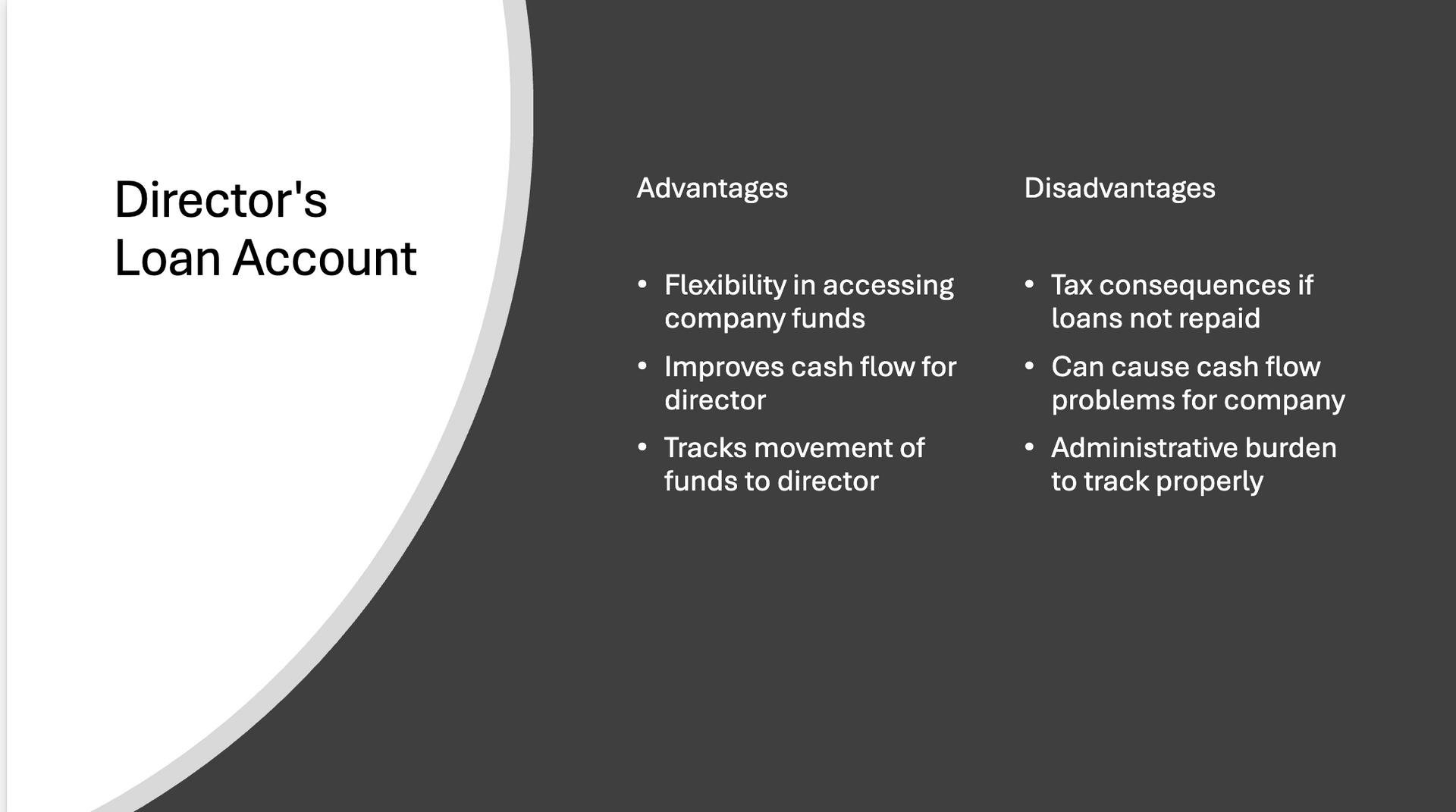

At the very least, the proposal when enforced, will mean closer controls on how money is transferred to directors and shareholders from their limited company, specifically via their director's loan account (DLA), although transfer of assets and other transfers of value are being included.

In short, what does an owner/director need to do?

If you are a contractor or director of a close company using the low‑salary plus dividends model, and making regular drawings in lieu of a dividend (a share of the company profits after corporation tax is calculated) now is a good time to:

- Review how you actually take money out of the company (salary, dividends, expenses, “drawings”) and check that it matches what your accounts and tax returns say.

- Tighten up your records: keep a clear, up‑to‑date Director’s Loan Account, minute dividend declarations properly, and retain supporting accounts (e.g. retain a Profit & Loss report as at end of month before the drawing to be treated as a dividend) to show there were sufficient profits in the company.

- Separate personal spending and company spending, so that it is always clear whether a payment is salary, a dividend, a loan, a reimbursed expense or a personal expense. Personal spending should be booked to a separate personal expenditure account, not the DLA.

- Move away from “we’ll sort it at year‑end” and get into the habit of updating DLAs and dividend paperwork in real time or at least monthly if drawings in lieu of dividends are taken out monthly.

- Speak to your accountant or tax adviser about whether your current strategy and record‑keeping would stand up to closer HMRC scrutiny under the proposed reporting regime.

You do not need to change everything overnight, but you do need to assume that HMRC will soon expect better, more regular information on how you pay yourself and so do plan accordingly.